Electronic invoicing between taxable persons (“e-invoicing”) and transmission of information (“e-reporting”) to the French tax authorities from 1 July 2024

From 1 July 2024, businesses will face new procedures for the transmission of invoices (“e-invoicing”) and transaction data (“e-reporting”).

The application of one and/or the other procedure will depend on the place of establishment of the parties, the territoriality rules allowing to determine whether the transaction falls within the scope of application of French VAT, as well as the applicable invoicing rules.

The expected objectives of this reform are to provide the tax authorities with additional means of combating fraud, to reduce the administrative burden on businesses linked to invoicing, to make it possible to automatically pre-fill VAT returns and to have real-time information on the economic activity of businesses, enabling the authorities to implement economic actions.

The following details are limited to outlining the scope of this major reform for businesses.

E-invoicing

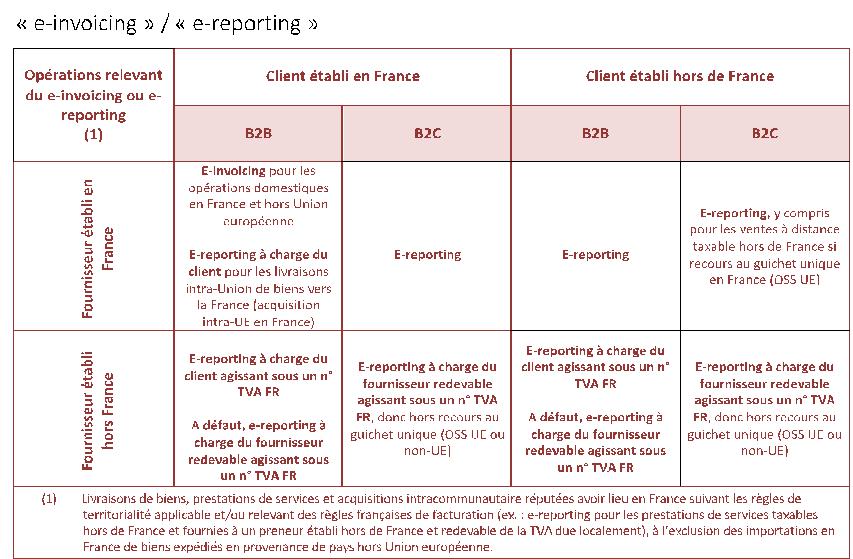

The new procedures for the transmission of invoices concern businesses established in France (metropolitan France and the departments of Guadeloupe, Martinique and Reunion) in respect of sales of goods and services supplied to their taxable customers (B2B) established in France, provided that these sales fall within the scope of French VAT and/or are subject to the invoicing rules applicable in France (Article 195 of the Finance Act for 2021 and Order No. 2021-1190 of 15 September 2021 amending Article 289 bis of the General Tax Code).

The e-invoicing procedure therefore only concerns situations where the supplier potentially liable for VAT in France and the customer are both taxable persons established in France. Thus, taxable transactions in another EU Member State, in which a company established in France would be identified for VAT purposes for the purposes of these transactions, do not fall within the scope of e-invoicing (nor within the scope of e-reporting).

For these transactions, companies will have to send their invoices electronically (e-invoicing) via a public invoicing portal (Chorus Pro) or a partner dematerialization platform chosen by the company. They will therefore no longer be able to send their invoices directly in paper or electronic format to their taxable customers established in France. These invoices will be issued, transmitted and received in dematerialized form and will contain certain data in structured form (which differentiates them from “paper” invoices or in PDF format). It is the platform that will transmit the invoice to the customer’s platform (or to the customer directly if he is on the same platform). The invoice is therefore transmitted via the platforms which transmit the invoice data to the tax authorities. A directory will list the French companies covered by the e-invoicing obligation and will indicate the choice of partner platform(s) for each of them.

The issue of invoices in PDF format will be accepted for the time being, on the understanding that subsequently the issue of invoices in a structured format will become mandatory. The tax authorities are currently examining the possibility of using the “Factur-X” format.

E-reporting

In the case of transactions not covered by the e-invoicing procedure – e.g. sales to private individuals (B2C) or legal entities under public law (B2G), imports of goods from third countries, sales to companies or private individuals not established in France (including the Principality of Monaco), sales by suppliers not established in France but liable for French VAT, etc. – companies will have to transmit certain transaction data (e-reporting) to the tax authorities, in accordance with the same terms and conditions as those applicable to electronic invoicing.

Suppliers established outside France are only concerned by the e-reporting obligation if they carry out transactions deemed to be located in France for which they are liable for VAT. Examples are taxable persons not established in France who carry out certain supplies of services in France and supplies of goods from France to another taxable person not established in France, where the customer is a company that does not have a VAT identification number in France. For sales to private individuals (B2C), the e-reporting obligation applies to the non-established supplier unless he declares his transactions through an European One-Stop Shop (EU or non-EU OSS).

Companies established in France dealing with a supplier established outside France will also have e-reporting obligations in respect of their domestic purchases of goods and services and intra-Community acquisitions of goods, but excluding imports from outside the EU.

The respective scope of the e-invoicing / e-reporting obligations for transactions deemed to take place in France under the applicable territoriality rules and/or under French invoicing rules can be summarized as follows

The administration will allow companies to submit electronic invoices to the intermediary portal even if this is not compulsory (e.g B2C) in order to facilitate the transmission of data to the administration in a structured (and not manual) manner. The portal will take care of transmitting the relevant data to the administration. This is only one way of transmitting data, as it remains within the scope of e-reporting.

The scope of the data to be transmitted in the context of e-reporting will in principle be reduced and will only concern the amount of turnover of the day’s transactions (amount excluding tax, VAT rate and data linked to the technical transmission of information).

Finally, for supplies of services for which the VAT collected by the supplier becomes due at the time of payment, the e-reporting obligations will include payment data (date of collection and amount collected including VAT, broken down by VAT rate where applicable). This procedure also concerns payment data for services covered by the “e-invoicing” procedure.

Scope of the new measures

This reform does not change the scope of invoicing so that operators already exempted from invoicing on their services are not covered by the e-invoicing and e-reporting procedure on these same services (e.g.: exempted transactions in the field of health, education and training services, real estate transactions, transactions carried out by non-profit associations, banking and financial transactions, insurance and reinsurance transactions).

As regards the content of invoices, however, the list of compulsory information to be included on the invoice will be supplemented by four additional items (including the customer’s VAT number).

Finally, the new rules have no impact on invoicing deadlines. Similarly, companies will still be required to keep and archive invoices.

Entry into force

As of 1 July 2024, all companies established in France, regardless of their size, will have to be able to receive electronic invoices, i.e have chosen a dematerialization platform.

As regards sales invoices, the new measures will come into force according to a timetable established according to the size of the issuing company: from 1 July 2024 for large companies, from 1 January 2025 for medium-sized companies and from 1 January 2026 for small and medium-sized companies.

It is understood that as of 1 January 2024, intermediate companies and small and medium-sized companies will be free to issue electronic invoices by complying with the new transmission modalities in advance if their partner is already subject to them or is voluntarily complying.

What actions need to be taken?

It is advisable to measure the issues and consequences of the reform according to the type of operations of your company (place of establishment of the parties, applicable invoicing rules and territoriality of the operation), and assess the steps to be taken in terms of organizing information systems (e.g to take account of changes in invoice content), relations with customers and suppliers, specifications for dematerialization platforms, updating the “reliable audit trail” documentation to justify the link between the invoice data and the underlying transactions, etc.